Why There Won't Be A Banking Crisis But We Need To Jail Some Of The VCs...

It’s not a banking crisis but it is a geopolitical one

My favorite true crime podcast is “All In.”

I dare not listen to it fully lest it encourage me to pump and dump stocks with the mob gang. Did you know that Jason Calacanis (through his father) and David Sacks (through his wife) have credible ties to organized crime?

Anyway I do happen to catch the clips. Who could miss them?

Sacks is often wrong. Here he’s being wrong again.

Or is he more menacingly trying to cause banking crises?

Is he, in other words, trying to pull a Canadian truckers op?

Of course when you look closely at all the banks affected you can see these banks have massive exposure to being on the wrong side of the Ukraine war.

No, it’s not like the banks did it but their depositors certainly picked the wrong side. Perhaps they weren’t even banks at all.

Put simply the way a lot of smaller banks make money is by avoiding the regulations that plague the larger banks.

Everybody wants to be a big bank regulated like a small bank. The bigger the bank gets, the more it has to do politics — and the less it cares about the local community.

But how do you become a big bank? You take a lot of foreign money or mega rich people money — but I repeat myself — that won’t ask too many questions. You give these people VIP banking services. You look the other way on know your customer laws. You market your deviations from the law and good banking practices as being “founder friendly.”

Other larger banks might ask questions about why you got a wire from say, China, but not these Chinese-compromised banks.

The “large phenomenon” was that each of these failed banks was on the wrong side of the Ukraine war.

You absolutely can do a network analysis of each of these banks. You can look at their depositors. You can look at their boards. You can look to their executive team.

This fact portends very poorly for David Sacks whose own venture fund looks increasingly like a front.

Let’s take these banks one by one.

Silvergate (California-Chinese)

Silvergate was deeply connected with cryptocurrency which is, “an attack on the U.S. dollar” as Peter Thiel once said. That is, before he encouraged people to buy bitcoin while he was selling it.

Silicon Valley Bank (California-Chinese-Israeli)

Madoff had a legitimate side to his business, too, but there’s mounting evidence that Silicon Valley Bank wasn’t a bank or even particularly based in Silicon Valley. When Silicon Valley Bank’s chief auditor John Peters worked for an Israeli company his job was to more closely integrate Silicon Valley Bank with China, India, and Israel.

Signature Bank (New York-Israeli)

Signature Bank was started in 2000 by Israeli bank, Bank Hapoalim, which sold its stake in 2005. The bank proceeded to get heavily involved in cryptocurrency.

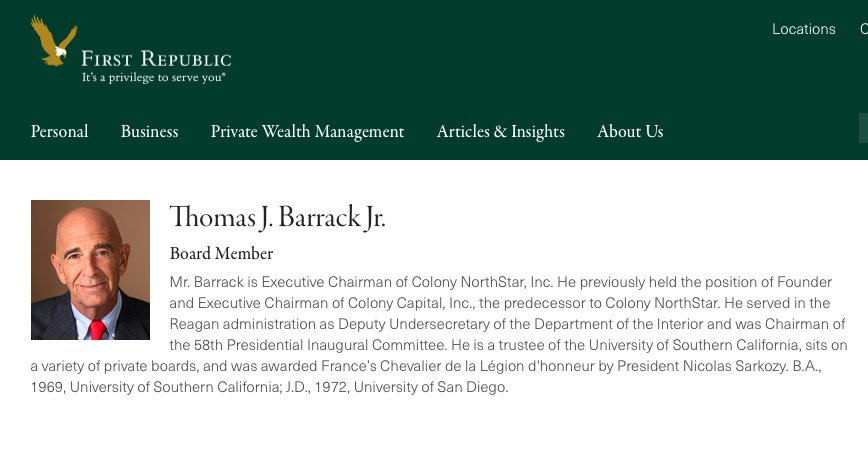

First Republic Bank (Russian-California-Chinese)

Did you know that disgraced alleged Emirati spy Tom Barrack was on the board of First Republic? Or that Michael Cohen banked all the bribes he was paid at First Republic? Cohen was also working very closely with Russian oligarch Viktor Vekselberg. First Republic Bank had all kinds of real estate exposure with the Chinese in San Francisco too.

Credit Suisse (Russian)

For many years the Russians have tucked their stolen money in Swiss bank accounts. That no longer became tenable after Putin invaded Ukraine. When the Swiss say that its $8 billion of frozen assets is “only a fraction of the total” while prosectors are charging Swiss bankers with overlooking moving millions of Putin-connected cash you know things are about to get wild in the normal staid Switzerland.

Apropos of nothing in particular: did you know, by the way, that Peter Thiel worked for Credit Suisse from 1993-1996?

****

My sense is that Matt Yglesias is right. We will ultimately end up with a number of regional banks and those banks’s successes and failures will more or less track with the fortunes of those regions of the country.

I suspect it was a mistake to force the larger banks to buy these failed banks right away. It should have been done slowly and carefully. What’s the hurry anyway?

Candidly I think we should go depositor by depositor and ask the obvious question about Silicon Valley, Signature Bank, et al.

Is this “innovation” — or espionage?

Blanket coverage for SVB depositors was not a good move , without a requirement for those rescued funds to be redeployed in AUKUS type interests